Demand for electric vehicles in Germany

Sales of electric cars in Germany are booming – and European governments are relying on incentives to make the switch easier and more affordable. A current example is the 2026 e-car subsidy, which provides significant subsidies for owners of electric vehicles in Germany.

To check how electric car adoption relates to charging infrastructure and government subsidies in Germany, we evaluated the complete vehicle registration data for 2025 for all federal states to measure the nationwide growth of electric vehicles. In addition, we used city-level data on electric car adoption and public charging stations from January 2025 to compare regional differences.

Status of electric car registrations in Germany

In 2025, more than 544,800 new electric vehicles were registered nationwide – this corresponds to a whopping 32% of all new registrations. Since the beginning of the year, growth has been rapid: On January 1, 2025, 1.65 million electric vehicles were registered, a share of 3.3%.

Nevertheless, gasoline vehicles remain the most common category with 777,442 new registrations in 2025, but the gap to electric vehicles is shrinking significantly. Registrations of diesel vehicles continue to decline: 394,718 new diesel cars were registered in 2025 – electric vehicles are now clearly between the two traditional drive types.

To enable a fair analysis, we examined the share of electric vehicles in all vehicles for each state in 2025. In the whole of 2025, Thuringia recorded the weakest registration figures for electric cars, with 21% of new cars in 2025 being electric vehicles. Saxony, Saxony-Anhalt and Mecklenburg-Western Pomerania follow with the second-lowest share of electric cars, with 23% of new cars in 2025 being electric vehicles.

The federal states that lead the way in electric vehicle registrations in 2025 include Baden-Württemberg with a share of 37% of new registrations (84,297), Berlin with 11,666 newly registered electric vehicles (37%) and Bremen (36%) with 3,264 electric vehicles.

In terms of the number of newly registered electric vehicles alone, North Rhine-Westphalia led the way with 116,529 new electric vehicles in 2025 (34%). Bavaria followed closely behind with 115,631 registered electric vehicles in 2025 (31%). Despite the high population of these provinces, the percentages are still quite high compared to other provinces.

Germany's pioneer and laggard in the field of electric vehicles

To find out which federal states have significantly increased or are lagging behind in the adoption of electric vehicles, we analyzed data from cities from January 2025 and compared it with data from the whole of 2025.

How do the 20 largest cities in Germany compare?

Below are the 20 largest cities in Germany and their share of electric vehicles in January 2025:

Stuttgart – 6% EV ownership

At the beginning of 2025, Stuttgart was at the top of Germany in terms of the share of electric vehicles: 6% of all registered vehicles were electric. With 2,118 public charging points, the city has 8.5 electric vehicles per charging point – one of the best values among the largest cities. At the same time, Stuttgart has a very high per capita penetration of 29.3 e-vehicles per 1,000 inhabitants. However, the proportion of fast-charging points is comparatively low at 5%.

Munich, Frankfurt am Main, Dusseldorf, Bielefeld and Bonn – 5% EV ownership

These cities each achieve an EV share of around 5% (as of January 2025), but differ significantly in charging coverage:

- Frankfurt am Main has 14 electric vehicles per charging point and 21.5 EVs per 1,000 inhabitants.

- Düsseldorf has 11.8 EVs per charging point and 25.5 EVs per 1,000 inhabitants.

- Bonn has a slightly lower charging point density of 17.5 EVs per charging point, but reaches 28.5 EVs per 1,000 inhabitants.

- Despite high EV penetration (25.9 EVs per 1,000 inhabitants), Bielefeld stands out for its comparatively high load on the charging infrastructure: 24.8 electric vehicles per charging point, but with the highest fast-charging share of this group (36%).

- Munich has the largest charging network within this group, but has 17 electric vehicles per charging point – an indication that the strong EV growth is increasingly demanding the infrastructure.

Hamburg, Cologne, Hanover, Nuremberg, and Mannheim – 4% EV ownership

With an EV share of around 4%, these cities are showing solid early adoption, with some very different infrastructure values:

- Hamburg has 2,475 charging points, but here there are 14.4 electric vehicles per charging point, with 19.1 EVs per 1,000 inhabitants.

- Cologne has 15.1 EVs per charging point, but offers a high proportion of fast charging points at 23%.

- Hanover stands out: Despite a 4% EV share, the city has 23.5 electric vehicles per charging point, but at the same time 40.1 EVs per 1,000 inhabitants – the highest per capita value in the entire comparison.

- Nuremberg (12.6 EVs per charging point) and Mannheim (12.2 EVs per charging point) have a comparatively balanced charging coverage with moderate EV density.

Berlin, Leipzig, Dortmund, Bremen, Essen, Bochum and Wuppertal – 3% EV ownership

With 4,287 charging points, Berlin has the largest charging network in Germany. With 9.8 electric vehicles per charging point, the capital has one of the best coverage rates, although the EV share is still comparatively low at 3% (11.4 EVs per 1,000 inhabitants).

- Leipzig (9.2 EVs per charging point) and Duisburg (9.9 EVs per charging point) also show good infrastructural coverage with low EV density.

- Dortmund (11.2 EVs per charging point) and Bremen (10 EVs per charging point) are in the solid midfield.

- Bochum and Wuppertal stand out for their very high shares of fast charging points (28% and 30% respectively), while at the same time the charging infrastructure there is more utilised – especially in Wuppertal with 25.1 electric vehicles per charging point.

Dresden and Duisburg – 2% EV ownership

Dresden recorded an EV share of 2% at the beginning of 2025, but with 31% fast charging points, it offers an above-average future-oriented infrastructure. At 10.5 electric vehicles per charging point, charging coverage is currently still good, while EV penetration remains comparatively low at 9.4 per 1,000 inhabitants.

With 527 public charging points and 9.9 electric vehicles per charging point, Duisburg currently still has comparatively good charging coverage. At the same time, EV penetration of 10.4 electric vehicles per 1,000 inhabitants is well below the level of many major West German cities. The share of fast charging points is 18%, which puts Duisburg in a solid position in terms of infrastructure, but which means that additional expansion is expected to be needed if the number of registrations continues to rise.

Federal states with large increase in electric vehicles in 2025

While the data at the city level show how demand and charging infrastructure were at the beginning of the year, the registration data at the state level provide information about where electromobility has gained particularly strong momentum in 2025 – and how well the infrastructure is keeping pace:

Berlin

In Berlin, the share of electric vehicles was only 3% at the beginning of 2025, but over the course of the year, electric vehicles accounted for 37% of all new registrations. With 3.2 newly registered EVs per 1,000 inhabitants, Berlin is in the middle of the field nationwide, but benefits from a very high infrastructure density: 4.8 charging points per km² – by far the highest value of all federal states. This means that Berlin is well prepared for further growth in terms of infrastructure, even if per capita demand is still comparatively moderate.

Baden-Württemberg

At the city level, Stuttgart will be at the top of Germany's major cities at the beginning of 2025 with a 6% EV share. This trend is also reflected nationwide: 37% of all new registrations in Baden-Württemberg in 2025 were electric vehicles, which corresponds to 7.5 new EVs per 1,000 inhabitants.

In relation to the area, however, the charging infrastructure is less dense: With 0.48 charging points per km², Baden-Württemberg lags behind city states and more densely populated regions. In addition, only 19% of charging points are fast chargers, which could lead to bottlenecks if demand continues to rise, especially on longer distances.

North Rhine-Westphalia

North Rhine-Westphalia shows a similar picture: Cities such as Düsseldorf, Bonn and Bielefeld were already at around 5% EV share at the beginning of 2025. Nationwide, electric vehicles accounted for 34% of new registrations in 2025, which corresponds to 6.5 new EVs per 1,000 inhabitants.

With 0.6 charging points per km², NRW has comparatively good area coverage. The fast-charging share is 24%, which puts the state in a solid position in terms of infrastructure, even if regional differences between metropolitan areas and rural areas remain.

Federal states with a need to catch up

Hamburg

Hamburg recorded a lower EV share of new registrations in 2025 than many other regions: 25% of newly registered vehicles were electric, which corresponds to 7.2 new EVs per 1,000 inhabitants.

Although the city-state has a high infrastructure density of 3.3 charging points per km², only 18% of the charging points are fast chargers. This means that Hamburg lags behind comparable city states such as Bremen in terms of both demand and fast-charging coverage.

Saxony

Saxony continues to be one of the federal states with slower EV dynamics. Cities such as Dresden and Leipzig already had low EV stocks at the beginning of 2025, and this trend continued: only 23% of new registrations in 2025 were electric vehicles, which corresponds to 3.0 new EVs per 1,000 inhabitants – one of the lowest values nationwide.

At 0.19 charging points per km², the infrastructure density is also comparatively low. Although the share of fast charging is relatively high at 31%, the low area coverage indicates that charging points outside the larger cities remain difficult to access.

Are charging stations keeping pace with the growing demand for electric vehicles?

The increasing number of electric vehicles is increasing the demand for public charging infrastructure, and data from cities shows significant differences in charger availability and charging speed.

Worryingly, the states with the highest number of electric vehicles also have the lowest availability of fast charging stations, which can lead to pressure and potential frustration among drivers. For example, Baden-Württemberg and Berlin have the highest number of newly registered electric vehicles, but only 19% (Baden-Württemberg) and 14% (Berlin) of fast-charging stations.

The data suggests that states with the highest demand for electric vehicles could be under significant pressure, especially if the number of electric vehicle registrations continues to rise.

The role of the new e-car subsidy

In January 2026, Germany introduced a new subsidy program for electric vehicles, which is intended to promote the purchase of electric vehicles through targeted financial support. The program provides for around 3 billion euros and supports around 800,000 vehicles by 2029. The subsidy applies retroactively to eligible vehicles that have been registered for the first time since the beginning of 2026.

However, a survey conducted by us among potential car buyers in Germany shows that there are still significant gaps in knowledge about the new subsidy program. Only 48% of respondents say they understand exactly how the funding applies to them personally. More than half (52%) feel only partially informed or are unsure whether they are eligible for funding at all.

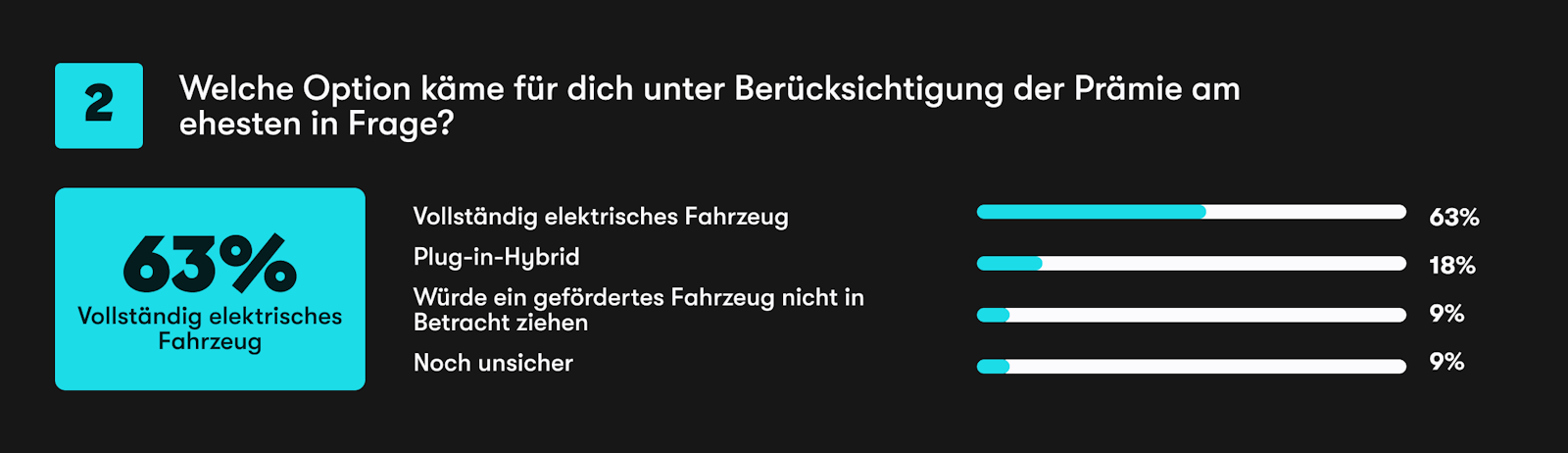

In addition, 63% of respondents said they prefer all-electric models, while 18% prefer plug-in hybrids. On the other hand, 9% say they are not considering buying an electric vehicle, and 9% are still undecided.

This development is also reflected in actual user behavior – at least on Carwow.de. Internal data on customer inquiries shows that in the first two weeks since the official announcement of the subsidies, requests for electric vehicles on the Carwow platform have increased by 268% compared to the two weeks before. Year-on-year, EV inquiries are 227% higher, while gasoline inquiries are down 22% and diesel are down 46%.

The total share of EV inquiries on Carwow increased from 40% to 72% year-on-year, and almost three-quarters of all inquiries are related to electric cars.

The data refers exclusively to user inquiries on Carwow and does not allow any conclusions to be drawn about the entire German car market, but clearly shows how strongly the subsidy program can influence demand within digital car buying platforms.

What does this mean for drivers?

In areas where the spread of electric vehicles is increasing rapidly, the demand for charging infrastructure for electric mobility is increasing, especially in locations with fewer fast charging stations. In cities with less prevalence of electric vehicles, the pressure on the availability of charging stations is less acute, but the charging station networks there are usually less well developed overall.

When choosing an electric vehicle, we recommend not only considering the cost of the vehicle. Regional aspects are important, so you should consider the charging stations in your city, the charging speed, the range and the possibility of charging at home. This will ensure that your electric vehicle is a cost-effective and practical choice for everyday use.

Conclusion

As we have already seen, the demand for electric vehicles increased rapidly throughout Germany in 2025. Our data show that the infrastructure is developing at different speeds in the different regions and that there are significant differences between the federal states in terms of the availability of charging stations and the charging speed. Since many leading federal states offer the lowest availability of fast charging stations, it will be interesting to observe how the charging infrastructure in Germany will develop in the next few years.

Methodology

For this analysis, the spread of electric vehicles and the expansion of the charging infrastructure in Germany at the city and state level were examined. It is based on publicly available, official data sets from government and recognized statistical sources, as well as a survey conducted among Carwow's customers. .

Population data

The population figures of major German cities and the population distribution by federal state are based on data from Statista.

Vehicle stock and new registrations

Data on the number of vehicles in Germany and new registrations in 2025 were taken from publications of the Federal Motor Transport Authority (KBA). The evaluation includes:

- the total number of registered vehicles,

- a breakdown by type of drive (petrol, diesel, electric),

- as well as new registrations in 2025 by state and drive type.

The share of electric vehicles was calculated as a percentage of the total number of vehicles or new registrations.

Charging infrastructure

Information on the public charging infrastructure comes from the charging station map of the Federal Network Agency. The following were taken into account:

- the total number of public charging points,

- the number of fast-charging points,

- as well as the share of fast chargers at all charging points.

The charging points were allocated on the basis of the reported locations within the respective cities or federal states.

Calculations and evaluations

On the basis of the merged data sets, the following key figures were calculated, among others:

- Share of electric vehicles in the vehicle fleet per city,

- Share of electric vehicles in new registrations in 2025 per federal state,

- number of electric vehicles per public charging point per city,

- share of fast charging points in the overall charging infrastructure,

- Rankings of the largest German cities by e-car share.

All percentages have been rounded commercially.

Survey results:

The survey was conducted internally by Carwow in January 2026 and was answered by more than 1,000 Carwow users.

source : https://www.carwow.de/automagazin/elektroauto/elektroauto-fahren/neuzulassungen-und-nachfrage-elektroautos-deutschland

Posting Komentar